+91 7738 0716 11

+91 7738 0716 11 +91 7738 0716 11

+91 7738 0716 11

Intellectual Property: Registration and Effects

by: Adv. Kishan Dutt Kalaskar 2023-03-30 16:34:46

by: Adv. Kishan Dutt Kalaskar 2023-03-30 16:34:46

by: Adv. Kishan Dutt Kalaskar 2023-03-30 16:20:33

by: Adv. Kishan Dutt Kalaskar 2023-02-28 18:47:16

by: Adv. Kishan Dutt Kalaskar 2023-02-28 18:10:41

by: Adv. Kishan Dutt Kalaskar 2023-02-03 22:32:13

by: Admin 2023-02-01 16:45:35

Intellectual Property: Registration and Effects

Clearance to get a Passport and Visa during the pendency of Criminal Cases

Summary of the Payment and Settlement System Act, 2007

Procedure to track court cases online

Key Features of Union Budget 2023

Top 10 reasons to hire a Civil Lawyer

5 Benefits Of Hiring A Business Lawyer When Starting Your Company

Top 5 Reasons Why You Should Consult A Banking Lawyer

10 Things to Consider Before Hiring an Accident Lawyer

Payment Recovery Process

Analyzing legal and security issues in cyber contracts (E - contracts)

Discharging and Quashing in Criminal Cases

Legal compliances for online shopping sites in India

How to select a Lawyer

Supreme Court Judgments 2022

Maternity Benefit Act 1961, at a Glance

Modes of Recording Accepted by Court

Essential elements of a sale under the Transfer of Property Act

Compensation in Motor Vehicle Accident Cases

Is it important to respond to a summon?

Analysis of Section 18 of Limitation Act, 1963

Fresh period of Limitation

The breakdown of the doctrine of Res-Judicat

Impact Of Supreme Court Ruling

Analysis of Employees Provident Fund and Miscellaneous Provisions Act

How is 'BLACK MAGIC' governed in India

Different Identities of an NDA

Breaking down the requirements of becoming a Public Prosecutor in India.

Mohan Breweries & Distilleries V/s Commercial Tax officer, Madras

Kavita Kanwar Vs. Mrs Pamela Mehta & Ors

Entry into Judiciary: Minimum required Qualifications

Law of Retrenchment

Grounds for refusal of a Trademark Application

Early disposal of pending cases by the High Court

Parminder Kaur V/s State of Punjab

Central Bank of India V/s M/S Maruti Acetylene Co. Ltd.

Goan Real Estate and Construction Ltd. And Anr. V/s Union of India

Raj Kumar V/s Ajay Kumar

Synopsis of the Special Marriage Act in India

Lok Adalat has no jurisdiction to decide a matter on Merits

Significance of a Police Clearance Certificate in a pending Accident Case

Understanding the Digital Rupee

Eligibility of Teachers for Gratuity under the Payment of Gratuity Act, 1972

Dr. M. Kocher V/s Ispita Seal

Smt. Seema Kumar V/s Ashwin Kumar

Leo Francis Xaviour V/s The Principal, Karunya Institute

Nazir Mohamed V/s J. Kamala and Ors.

Addissery Raghavan V/s Cheruvalath Krishnadasan

Himalaya House Co. Ltd. Bombay V/s Chief Controlling Revenue

K. Sivaram V/s P. Satishkmar

Basir Ahmed Sisodia V/s The Income Tax Officer

Burden of Proof

Interest for delayed Payment under Payment of Gratuity Act, 1972 - Need for Change?

How to file a complaint in regards to violation of Cyber Laws

Delayed Justice from Consumer Courts

Can a registered Will be challenged in the Indian Court?

Trademark Infringement - Triple identity test in Trademark

Blockchain Technology in India – II

Manish V/s Nidhi Kakkar

Withdrawal of Mutual Divorce Proceedings

Blockchain Technology in India - I

Unnatural Offences

Surendra Kumar Bhilawe V/s The New India Assurance Company

Seat Vs Venue of Arbitration

D. Velusamy V/s D. Patchaimmal

Standard from of Contract - Legal or Illegal?

Life Insurance Corporation of India V/s Mukesh Poonamchand Shah

MSME Debt Recovery Provisions

Neelam Gupta Vs Mahipal Sharan Gupta

Analysis of Section 11A of Industrial Dispute Act, 1947.

Time Limits & Procedure to approach HC in Civil Cases

The necessity of Gender-Neutral laws in India

Sou. Sandhya Manoj Wankhade V/s Manoj Bhimrao Wankhade

Plea of Adjustment

Filing of Complaints against biased Judges

G. Raj Mallaih and Anr. V/s State of Andhra Pradesh

Zee Entertainment Enterprise Ltd. V/s Suresh Production

Chief Administrator of Huda &Anr. v/s Shakuntala Devi

Permanent Child Custody

Dilution of the statutory protection available to MSMEs

Validity of an Unregistered Sale Agreement

Ambalal Sarabhai Enterprise v/s Ks Infraspace LLP

False and misleading advertisements in India

National Legal Service Authority v/s Union of India and Others

Recovery Procedure in Cheque Bounce Cases

Roxann Sharma V/s Arun Sharma

Ganesh Santa Ram Sirur V/s State Bank of India &Anr.

Recovery Procedure of Consumer Court Cases

Bank Guarantee

M/s M.M.T.C Ltd. & Anr v/s M/s Medchl Chemical & Pharma P

Shailendra Swarup V/s Enforcement Directorate, The Deputy

SunitaTokas v/s New India Insurance Ltd.

Can couples get separated without a divorce?

Scope of Arbitration in India

Appointment of Arbitrators

NRIs right to purchase Property in India

Decriminalization of Dishonour of Cheques: a measure contradictory to its purpose

Paternity leave in India

Regulation of Cryptocurrency in India

How can litigants list their cases online?

Validity of Narco-Analysis in India

Remedies against frivolous cases registered against students by the Police

Procedures involved in a Criminal Trial

Procedured Involved in a Family Court Case

Death Certificate of a missing Person

Accountability of Police

Highlight of important Dishonour of Cheque case laws in 2020

Guidelines to be followed by Registered Medical Practitioners to dispense medicines

Land Mark Judgements on Family Law for the Year 2020

Remedies against harassment by Recovery Agents

Abetment to Suicide

Overview of the Vehicle Scrappage Policy

Rights of husbands in dowry and cruelty-based complaints

Admissibility of E-evidence; Are WhatsApp chats and E-mails admissible in Court?

Triloki Nath Singh V/s Anirudh Singh

Milmet Oftho & Ors. V/s Allergan Inc.

Director of Income Tax II (International Taxation) V/s M/s Samsung Heavy Industries Co. Ltd.

M/s ExL Careers V/s Frankfinn Aviation Services Pvt. Ltd.

The Maharashtra State Cooperative Bank Ltd V/s Babulal Lade & Ors.

Constitutionality of Bandhs

State of Himachal Pradesh V/s A parent of a student of a Medical College & Ors.

Rathnamma & Ors. V/s Sujathamma & Ors.

Ravinder Kaur Grewal V/s Manjit Kaur

Ficus Pax Pvt. Ltd. V/s Union of Indian & Ors.

Commissioner of Income Tax V/s Chandra Sekhar

Analysis of Section 41-A of CRPC, 1973

Judgment: Indian Bank V/s Abs Marine Product Pvt. Ltd.

Kailas & Ors. V/s State of Maharashtra

Sukhedu Das Vs Rita Mukherjee

Witness to a Will

National Insurance Co. Ltd V/s Hindustan Safety Glass Works

Mahalakshmi V/s Bala Venkatram (d) through LR & Anr.

Kajal V/s Jagdish Chand

Shyamal Kumar V/s Sushil Kumar Agarwal

NRI's Power of Attorney

Megha Khandelwal V/s Rajat Khandelwal and Ors.

Is Registration Compulsory under Trademark and Copyright?

Md. Eqbal & Anrs. V/s State of Jharkhand

Types of Will

Employment Contract

Police Clearance Certificate

Validity of Crypto-Currency in India

A. Jayachandra V/s Aneelkaur

Points to be considered before filing an Income Tax Return

Union of India V/s N. K. Shrivasta

Startup under the Government Programme

The procedure for filing a complaint against a Lawyer

Types of Stamp Paper

Satvinder Singh V/s State of Bihar

Sexual Violence laws under the Indian Penal Code

Shreya Singhal V/s Union of India

Division of Assets

Shaleen Kabra V/s Shiwani Kabra

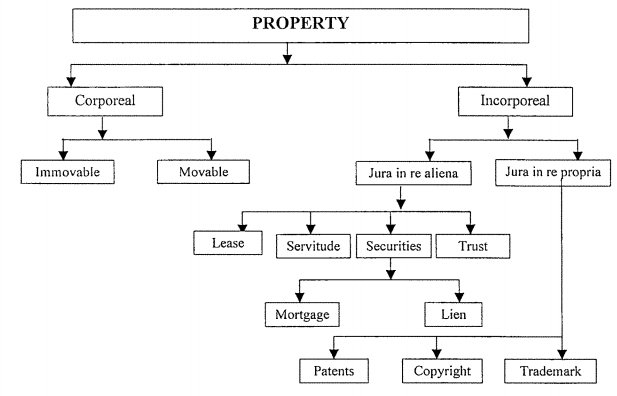

Types of Property

Vasant Kumar V/s Vijaykumari

Personal Injury - Damages

Adultery under the Indian Law

United Commercial Bank & Anr. V/s Deepak Debbarma & others

Intentional Wrongs

Vinay Kumar Mittal & Others V/s Deewan Housing Financial Corporation Limited

How to get a Marriage Certificate?

Mohammed Siddique Vs National Insurance Company Ltd

Pagdi System

The Bonus Act

Frivolous Complaints under the Sexual Harassment Act

Important Income Tax Return Forms and its Due Dates

Garden Leave

How can a Private Complaint be filed?

Key changes to Indian Tax Regulations

Employees Provident Fund

Status of Triple Talaq

Contract Farming & the new ordinances that affect the Farmers

Documents required for filing a Divorce

Section 138, 141 and 142 of the Negotiable Instrument Act 1881

Validity and Enforceability of Click-wrap Agreements

Child Custody under Christian and Parsi Law

Hindu Succession Act

Oppression and Mismanagement

Fraudulent and Invalid Contracts

Developments in Reserve Bank of India

Loan Frauds in India

Penalties associated with Driving

Laws governing a Knife

Medical Negligence and its Compensation

Interim Maintenance under the Domestic Violence Act

Shortcomings of the Consumer Protection Act, 2019

Tougher rules for the E-Commerce Industry

Difficulties faced by men in Family Courts

The consumer is the King in 2020

Illegal Termination of an Employee during Covid-19.

Child Labour Laws in times of Covid-19

Real Estate scenario Post Covid-19

Post Covid-19 Digital Shift of Legal practise

Mutual Consent Divorce through Video Conferencing

59 Chinese Apps banned in India

Litigants and the Lockdown - A Court Perspective

Anticipatory Bail for cases under section 498A of IPC

Brand Protection in times of Covid-19

Title Verification of Immovable Property

The Judiciary during the Pandemic

Termination of an Employee during Covid-19

Drafting of a Will

Criminal Medical Negligence in times of Covid-19

How does Covid-19 affect employers and employees?

Rent deference during the Pandemic

Post Covid-19 digital shift of legal practise

Police Interrogation

Prenuptial Agreements

Void and Voidable Contracts

The Negotiable Instrument Act 1881

Cheque Bounce Notice

Types of Dishonour of Cheques

Intestate Succession

The Stand of Essential Commodities

Trademark Cease and Desist Notice

IT Department Notice

Eviction of a Tenant

Consumer Complaint Legal Notice

Medical Adherence to Environmental Laws

Basic Elements of Transfer of Property Act, 1882

Debt Recovery Notice

Cheque Bounce Notice

Hygiene maintenance in Hospitals and Clinics

Consequences of using a Fake Degree/Certificate

Healthcare Security

Rights of Doctors with respect to Medical Negligence

Importance of Consent

Faulty Machine Aids Medical Negligence

The Special Marriage Act, 1954

Top 2019 judgements by Supreme Court

National Medical Commission Act 2019

Money Laundering

Hindu Undivided Family (HUF)

Child Labour

Endorsement under Negotiable Instrument Act

Quashing of an FIR

Annulment of Marriage

Probate

FAQ's on Trademark

EMI - Equated Monthly Installments

Legal mistakes made by the Start-Up

What is a Stamp Paper?

Sexual Abuse in Shelter Homes

Debt Recovery provisions under the SARFAESI Act

Effective ways to stop Ragging

Transfer of Property Act

Personal Injury Lawyers

Marriage Registration under the Special Marriage Act

Rights of Tenant

Classification of various Collar Jobs

Documents to be submitted for ITR Filing

Illegal Immigrants

Role of lawyers in Corporate Finance

Intestate Succession

Employment of White Collar Employment of White Collar

Domestic Violence

Power of Attorney

Dissolution of Marriage - Christian

Noting And Protest

Hostile Witness

Unfair Trade Practice

All you need to know: Drafting a Legal Notice

Fraudulent and unauthorized transactions at ATM

Is legal documentation important in medical practice?

Why do doctors need to be updated with medical negligence laws?

Personal Data Protection Bill, 2019

Jurisdiction of Consumer Redressal Forums

Does telephonic consultations amount to culpable negligence?

Consumer dispute Redressal Forum in dealing with Medical Negligence

Validity of Notices.

Response to a Legal Notice

Promotion of Medical Products.

Doctors' Bill: Prohibition of Violence & Damage to Property Bill, 2019.

Why less Indemnity cover is risky for Doctors?

Procedure for filing a Notice in India

Format of Legal Notices in India

Citizenship Amendment Act, 2019

Demerger

Legal framework for the Elimination of violence against Women in India

International Day for the Elimination of violence against Women

Family Courts in India

Inheritance Law in India

Rights of Children in India

Virtual Clinic

New Medical Technologies in India

Land Records & Titles

Regulations for firecrackers during Diwali

Legal and Regulatory Regime: Medical Technology

Intellectual Property in Medicine

Consumer Protection Bill, 2019

Artificial Intelligence in healthcare

The Real Estate (Regulation & Development) Act

Warrant and its Types

Joint Custody of Child in India

Limited Liability Partnership (LLP)

Penal Provision on Rash and Negligent Driving

National Company Law Tribunal

Rules to be followed by the Ganpati Mandals

Need to amend CrPC and IPC to increase the conviction rate.

Motor Vehicle Amendment Act, 2019

The Growth of technology Patents in India

Citizenship under the Indian Constitution

Basic Structure of the Indian Constitution

A comparative study of the Indian, UK and the US Constitution

Can the Indian Constitution be Amended?

Overview of the Indian Constitution

All you need to know: Drafting a Legal Notice

Surrogacy (Regulation) Bill, 2019

Overview of The Indian Penal Code

Offences and Prosecution under the Income Tax Act, 1961

The abolishment of Article 370 of the Constitution: One Nation One Flag

Intervention of SC in the Unnao Rape Case

Case of abandoned NRI brides, Supreme Court issues notice to the State

Financial Risk Management

Know more about Equal Remuneration Act, 1976

Procedure to File Complain against Domestic Violence

The IndiGo Promotors Feud

Rajya Sabha passes the Triple Talaq Bill

Gift Deed

More about Contested Divorce

Things to be kept in mind - Dishonor of Cheque

Prison Reforms in India

Consumer Protection ACT, 1986

More about Joint Venture

Delay of Condonation

Points to be Noted for Child Custody to Father

Basic information of Companies

Plastic Money and their Advantage & Disadvantages

Motor Accident Claim Tribunal

Guidelines to protect doctors from frivolous and unjust prosecution

Unjust Compensation - A Doctors Perspective

Misdiagnosis: A Medical Negligence?

Exemption of doctors operating in Emergency Rooms

General Types of Medico-Legal Cases (MLC)

Duty of patient to avoid aiding Medical Negligence

Rights of the Patient

Steps to be taken to avoid Medical Negligence

Liability of Medical Negligence under Consumer Protection Act

Laws that affect Medical Professionals in India

Defense against Medical Negligence Cases

Duties of Doctors

Common types of Medical Negligence

Medical Consent for treatment in India

Regulation for E - Pharmacy in India

Types of Consent for Medical Treatment

Guidelines for Autopsy/ Postmortem in India

Guidelines for the prescription of medicines

Procedure to start a Pharmacy Store in India

India Vs Pakistan: Kulbhushan Jadhav's Case

Contempt of Court

Juvenile Justice Act, 2000

Bankruptcy & Insolvency in India

The Maternity Benefit Act, 1961

Guardian and Ward Act In India

Medical Negligence in India

Procedure to be followed in Civil Recovery Proceedings

Rights of Consumers

Mandatory Registration of Documents and procedure

Rafale Deal And All About The Controversy

A bank guarantee is an assurance given by the bank to any third person wherein the bank agrees to undertake the risk of payment on behalf of the debtor to the creditor. The parties enter into a contract of guarantee, and the bank acts as a surety. Bank guarantees are commonly used for business and personal transactions and seek to protect the creditor from suffering any financial losses in case of default in payment by the debtor. This guarantee secures the creditors and helps businesses grow. Under a contract of bank guarantee, the creditor becomes the beneficiary and is entitled to claim the advanced amount from the bank. If the bank fails to fulfil its obligations under the BG, the creditor can proceed to bring an action before the Courts.

Validity period and claim period of a Bank Guarantee

The validity period is the period of existence or the lifetime of a bank guarantee (BG). A beneficiary (the creditor) can make a written demand to the bank in furtherance of the BG during the validity period. However, in certain cases, the BGs contain a clause that lays an additional period within which the claims can be made. This grace period is known as the claim period. Though it is generally expected that these dates are different, still there is no compulsion to keep both the dates different, as such, the expiry date of the claim period ranges from one to twelve months after the validity period.

Liability of banks upon invocation of bank guarantee

A bank that is a party to the BG undertakes an obligation to make payment when the beneficiary creditor makes a legitimate claim within the validity period of the concerned BG. By virtue of the contract of guarantee, a creditor becomes entitled to claim payment of the bank when the borrower defaults and can even enforce this claim before the Courts. Before making payment upon the presentation of a claim, the banks first notify the debtor of the same and requires them to arrange for funds to pay the claimed amount. However, if the borrower fails, the Bank has to pay.

In UP State Sugar Corporation Vs Sumac International Ltd, the Supreme Court held that when an unconditional bank guarantee is provided or accepted, the beneficiary is entitled to realize such bank guarantee regardless of the ongoing disputes and a bank guarantee constituted a bargain between the two parties, by which the bank unconditionally had to pay the amount in question.

Section 128 of the Indian Contract Act talks about the concept of a surety’s liability, and it states that the liability of the surety is co-extensive with that of the principal debtor unless it is proved otherwise by the contract.

In M/S Adani Agri Fresh Ltd Vs Mahaboob Sharif & Ors, it was highlighted by the Supreme Court that the bank guarantee is an unconditional one, and the respondent thus cannot raise any dispute and prevent the appellant from encashing the bank guarantee.

Similarly, in the case of Ansal Engineering Projects Ltd Vs Tehri Hydro Development Corporation Ltd, the Supreme Court stated that a bank guarantee is a separate contract entered into between a bank and a beneficiary and is not subject to underlying transaction and also that since the bank had unequivocally agreed to pay on demand, the liability of the bank was absolute and unconditional and could not be circumvented in any manner whatsoever.

When the question of liability of bank in case the beneficiary presents a claim during the claim period arises, one has to consider Section 28 of the Indian Contract Act, 1872. Section 28 lays down that any agreement in restraint of legal proceedings shall be void. However, exception 3 to this section saves the guarantee agreement of a bank or financial institution from the application of the general rule. Moreover, the Limitation Act, 1963 provides for a time limit of one year for a normal bank guarantee, but on the other hand, it has prescribed thirty years for all suits to be instituted by the government. This prescribed limitation period made the banks apprehensive about Section 28 of the Indian Contract, which before the amendment of 2013, had declared all agreements containing stipulation of discharge of liability as null and void.

Prior to 1997, the situation was that according to Section 28, any agreement through which any party was restricted from enforcing its right in respect of any contract by the usual legal proceedings in tribunal or even limited the time within which this could be done was void to that extent. It was in 1997 that an amendment to Section 28(b) of the Indian Contract Act was made to provide for agreements that extinguished the rights of any party or discharge any party from any liability under or in respect of any contract on the expiry of a specified period to restrict any party from enforcing its rights.

It can be seen through the judgement pronounced in Union of India v. Bhagwati Cottons Ltd, in which the Court held that any agreement containing a clause stipulating that rights of a party shall be suspended and another party shall be discharged from liability if the claim is not filed within the stipulated time, would be hit by the 1997 amendment.

Despite this decision by the Division Bench of the Bombay High Court, in the case of Explore Computers Pvt Ltd v. CALS ltd and Anr, the Court took a different stance by stating that though the clause within the agreements specifying the time limit within which beneficiary has to enforce its claim within sometime after expiry of bank guarantee is considered to be void in nature but the clause terminating the forfeiture or suspension of the right of claim is not brought within the specified time after the expiry of bank guarantee is valid.

In Union of India & Ors. v. IndusInd Bank Ltd & Ors, while upholding the validity of a clause limiting the claim period for the assertion of a right, the Supreme Court observed that it's clearly stated under the law that a clause that restricts the Limitation Period is not always hit with the aid of using Section 28 of the Indian Contract Act. The amendments to Section 28 are a substantive change in the law which provides that even where an agreement seeks to extinguish the rights or discharges the liability of any party to an agreement having the effect of restricting such party from enforcing their rights on the expiry of a stipulated period would be void to that extent.

It was because of these conflicting judgments that an amendment was brought in the Indian Contract Act in the year 2013, i.e. exception 3 to Section 28, which was responsible for providing validity to the clause in the contracts which provided for extinguishment of rights or discharge from any liability, the period of which should not be a less than one year from the date of occurring or non- occurring of a specified event. In the IndusInd case, it was held that the effect of this exception is to limit the period provided under the Limitation Act from three years to one year in the case of banks and financial institutions which issue a guarantee.

In the case of Kaushalya Rant v. Gopal Singh, it was held that Explanation 3 of Section 28 is dealing with a special branch, i.e. the Bank Guarantee and is confined to a specific branch and therefore, to that extent and in terms of statutory interpretation, exception 3 is a special law and as such would prevail over the Limitation Act, 1963.

Furthermore, the Reserve Bank of India, in a circulation dated 9th October 2015, has confirmed the 2013 amendment by stating that the Banks are not allowed to keep margin money after the invocation period.

Thus, the Banks may be discharged of their liability in the following two conditions:

Rights of Parties involved in Bank Guarantee

A Bank Guarantee is considered as a tripartite agreement between three main parties, namely, the principal debtor (the customer), beneficiary (the creditor) and the surety/guarantor (the bank).

Rights of Surety

All those rights made available to the parties to the contract are made available to the surety. These rights are as the following:

Rights of Beneficiary

As the surety's liability is co-extensive with that of the principal debtor, according to section 128 of the Indian Contract Act, then the beneficiary can sue the bank in case of default by the principal debtor to fulfil the liability.

Is default by performing party essential for invocation of guarantee?

Bank Guarantees are an exception to the general rule as contained under Section 126 of the Indian Contract Act that there must be default in performance by the performing party, and there is a need to establish a default on the part of the performing party by invoking party. To enjoy the benefits of invocation, the beneficiary in a BG needs to do it before the expiry date of the guarantee. If the bank does not receive any claim on or before the validity period, it is discharged from its liability. The beneficiary has to send a letter to the bank detailing the circumstances requiring the encashment of the guarantee.

In Maharashtra SEB v. Official Liquidator, the Supreme Court stated that the board has a right to enforce payment of guarantee as money is payable on demand and not on the breach. A bank guarantee is also called as ‘on-demand guarantee’ or ‘unconditional performance of guarantee’, which means that in any case, the bank is liable to pay without the need of the creditor to prove that any breach or loss occurred because of that breach. It was further held that in case of default by the debtor, the creditor could ask for performance, and the bank is bound to indemnify the creditor without default.

In Road Machines India (p) Ltd v. Projects & Equipment Corporation India, it was observed that the invocation of a bank guarantee must not necessarily be initiated with the aid of setting out the whole case in the form of a plaint with a definite cause of action and also that it was a commercial document, not a legal notice or a pleading. It is enough if there's substantial compliance regarding the guarantee within the notice issued.

Despite this, the government, in a separate stance to counter the problem of non-honouring of guarantees by the banks in cases related to government departments, has come up with the solution of advising their departments to invoke guarantees only after careful consideration of the fact that there is a default according to the terms and conditions specified.

Conclusion

Many BGs contain clauses providing for a claim period. Suppose the beneficiary presents a claim after the expiry of the validity period but within the claim period. In that case, the bank can still be obliged to pay but the obligations of the bank to make payment on behalf of the debtor ends with the expiry of the claim period.

Comment

Share